Nikko Asset Management: Navigating the Road Ahead for Global Equities

William Low, Portfolio Manager in Nikko AM’s Global Equity Team, explores the road ahead for global equities and the sectors likely to benefit. To learn more about the team’s investment approach you can download their new investment guide here.

In recent times, the experience of investing in risk assets has been a rather miserable affair for everyone involved—particularly in some corners of the market where we have seen an utter collapse in share prices. We wonder, however, why this was so surprising for so many investors.

The evidence would suggest investors have become conditioned by the benign environment that had been prevalent for more than a decade, creating a smooth and clear road to higher prices for equities and indeed most financial assets. The world’s key central banks had the specific goal of lower yields on financial assets since the great experiment of quantitative easing commenced. This post-financial crisis era has been less about investing capital and more about the ‘great inflation’ of financial assets.

Source: Getty Images

Source: Getty Images

This era even had its own language: SPAC, FAANG, meme, NFT, crypto, FOMO, and so on.[1] We live in a world where artificial intelligence is developing rapidly and is able to join the dots within larger data sets much better than humans can. We will, no doubt, underestimate the degree of future advances in this area. However, we should not underestimate the power of human thinking, as joining the dots on the wide array of evidence from different sources has been giving us valuable insights for some time.

As a global equity team, we are always discussing these observations and the insights they provide. In fact, they are instrumental both in directing our research towards the best new ideas and appraising our current investments. The valuation of companies has been a key area of focus, particularly since COVID-related monetary interventions pushed valuation disparities within equity markets to exceptional levels. In 2021, we wrote “These balloons…will not stay high in the sky…and the only debate will be the speed of descent”. Then in early 2022, we wrote “Make no mistake, there are many aspects of this that have the trappings of a bubble”. This is the human algorithm (or “Halgo[2]” for short) in action, and a good reminder to ourselves of the value of staying disciplined and bringing experience to the table. Being constructively critical is essential in today’s turbulent world.

All investors are now faced with a new and ongoing challenge. Policymakers no longer ‘have our back’, and inflation (rather than the price of risk assets) is now their number one priority. The road ahead is not going to be so easy for investors, but there are several useful steps they can choose to take.

Three steps for the new road ahead

It may be easy to become gloomy in the turbulence of today, but there are plenty of reasons for investors to be optimistic about the prospects for compounding future capital from today’s levels, provided the following three steps are taken into account.

1. Recognise that the road is rougher and more uncertain

Source: Getty Images

Source: Getty ImagesIn the shorter term, we expect a period of easing pressures as higher interest rates cool inflation (and result in lower growth) and supply chain pressures ease somewhat. However, on balance, structural energy undersupply, labour market constraints and military expenditures could all contribute to ‘sticky’ inflation at rates above the 2-3% ideal for central banks. Risk-free rates will therefore remain at higher levels for the foreseeable future.

Second, geopolitical uncertainty shows no signs of abating as the battles for technology hegemony between China and the US and Russia’s struggle for military supremacy in Ukraine continues. The free flow of capital across borders can no longer be assumed, the cost of borrowing in the US dollar – the world’s reserve currency – will likely stay high. Additionally, we need to be prepared for an increasing shift from China and other actors who intend to move away from the US dollar as the currency of external trade.

In short, we believe that growth in the broader economy will be less certain and more cyclical. As a result, we do not expect the cost of capital to return to the low levels seen in 2020–2021 any time soon.

2. Realise that this new road may be best travelled with different vehicles

The good, albeit challenging, news for investors is that when there is a regime change, as the significant market correction seems to flag, there is a high probability that there will be new leaders in the race ahead.

We have done some work on prior periods of significant market corrections and what the probabilities are, with a clear caveat that the number of reference data points is modest in total.

As a reminder, the leaders over the last cycle were the Information Technology, Consumer Discretionary and Energy sectors. Assuming they will automatically return as market leaders is a brave call based on this work. Our team’s view is that new leadership is likely to emerge this time, given the scale of surplus of capital that has just been allocated to those winners.

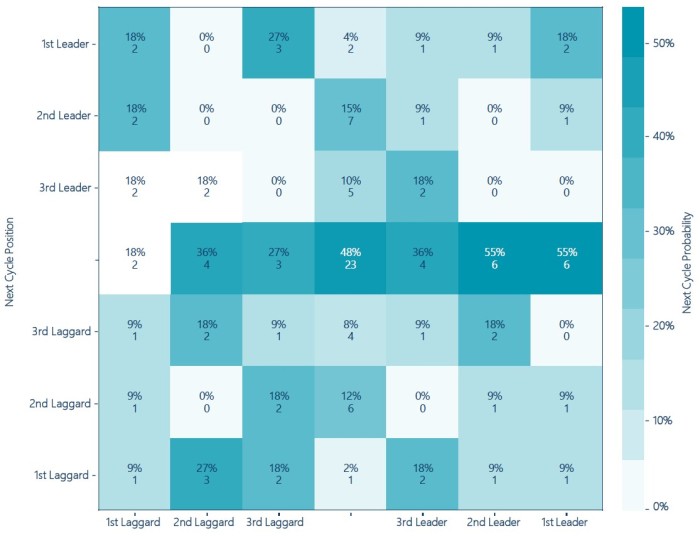

Figure 1: Market leadership in a historical context

Probability of maintaining leadership after market drawdowns greater than 20% (1957-2022)

Source: RENMAC

The above table looks at the probability of a sector in the equity market leading in the next market cycle having led in the previous one. We may all be familiar with the outsized gains made by the Technology sector in recent years, but after the 20% drawdown in markets in early 2022, what are the chances that a former market leader can repeat their outperformance in the next market advance?

This study ranks sectors for the US market back to 1957. It counts the bull cycle as the point of the price low after a 20% bear market to the subsequent price high before the next 20% drawdown. There were 11 such cycles in the last 65 years. The question “what is the probability of tech leading the market over the next five years or so” is answered in the top right of the table. The answer is just a 27% chance of tech being in the top two sectors for forward returns from here – in other words, it’s possible but less likely than one might expect. In fact, the top left portion of the table shows a higher probability that the next cycle could be led by those sectors that have lagged the most. This study underlines the need for investors to keep an open mind as to where market leadership will emerge.

3. Improve probabilities by sticking to a few enduring principles

Invest in price makers versus price takers

It is not just the price for assets that has had favourable tailwinds over the last decade, but also profitability. Profit shares as a percentage of GDP have been at record levels in most economies, and this has conditioned investor behaviour, with recency bias leading many to assume this will remain the norm. Work by empirical research previously highlighted that in the decade prior to 2021, about half of the improvement in profit margins for US manufacturers was down due to lower interest costs and taxes. While lengthening of debt duration may dilute the impact of rising rates, there is now a clear headwind for interest costs while taxes similarly are heading upwards in many economies.

Gross margins are also being challenged by rising labour inflation (and availability), a shift to more local and higher cost supply chains, rising raw material input prices, and (particularly for those sectors previously benefitting from COVID-related revenue boosts) negative operating leverage as sales decline. On average, times are getting tougher for businesses, and franchise strength is being tested more fully. Where products and business models are unique, dominant or gaining share, the scope for passing on costs to customers and sustaining volume growth is greater.

Ensure capital funding is sustainable

The cost of debt is going up notably, and as is always the case, the availability of debt could become more irregular. The degree of change in debt costs in US dollars is much greater than in other currencies, and given its reserve currency status this raises the global cost of capital for many businesses. In our view, self-funding growth (high free cash flow) and balance sheets with appropriate and long duration debt will be better placed to keep investing through down cycles. Cash-burning, profitless business models likely won’t pass the test.

Focus on justifiable valuations

We have learned, sometimes through bitter experience, that the penalty for investing at inflated prices and a lack of future cashflows is quite burdensome. Compounding of capital from levels that can be politely described as ‘frothy’ is really difficult. When the music stops, falls of 80-90% are common for the frothy crowd, and more often than not they stay down as profitability remains a dream rather than reality.

Where we find the ‘Future Quality’ winners

For more seasoned investors, none of the above should be particularly surprising. The next key question will likely be where to invest capital within global equities? In our view, companies on a unique journey of improvement that can attain and sustain high returns on invested capital over the next five years or more offer the best starting point. We call these ‘Future Quality’ companies, and they have been the foundation of our alpha generation for more than a decade. Here are the common traits shared by Future Quality companies:

Energy transition

Energy transitions take a long time. The first modern day energy revolution in the early 19th century, from wood to coal, fuelled great innovation that helped power the first railroads and ocean-going ships. The introduction of widespread electricity in the 1880s, led to inventions such as electric elevators, refrigerators and the mechanisation of agriculture. By the late 1920s, refined oil dominated the transport sector and reached a high point as a percentage share of all energy by 1973. Each transition required massive infrastructure spend before the benefits from adjacent technologies could be realised. These were ‘system’ changes, fighting incumbents and vested interests, and on average took 50 years before reaching maturation.

We are optimistic about the fourth energy transition as an investment theme, and believe that an enduring cycle of rising investment is now upon. Societies must address the challenge of sustaining the still-needed fossil fuel production, increasing supply from more trusted regimes, improving energy efficiencies, reducing emissions and developing alternative energy sources further. The latter is key from a climate perspective, but also energy-intensive in its own right, creating a circular requirement for the other drivers. In short, the addressable market will grow and surprise investors, and profitability for many suppliers of the “picks and shovels” of the energy transition is on an improving trend. This is an increasing rarity in the current environment.

Enduring growth

Given the environment of higher interest rates, and continued pressures on household consumption, we are increasingly cautious on the growth outlook for many consumer-facing companies. We believe that the falling propensity to consume (due to greater spending on mortgage and utility costs) and prior COVID-led pulling forward of demand will be difficult and enduring problems to overcome.

Sustainable growth that is less impacted by consumer cyclicality is therefore preferable. Our long-standing overweight in the Healthcare sector highlights that we see the demand for better and more cost-effective solutions across ageing societies as being a long-term positive. Healthcare companies typically have less cyclicality in demand and, in many cases, have been indiscriminately derated in the reappraisal of higher growth companies. We keep finding more Future Quality picks here, where confidence in growth is higher compared to other sectors.

One final comment on enduring growth is that we are increasingly concerned about the prospects for digital advertising. Business start-ups and the costs of funding for newer business models have ballooned in recent years, as conducive capital markets have enabled initial public offerings (IPOs), SPACs and a flurry of activity in private equity funding. In 2021, start-up funding was estimated at $650 billion in the US (Source: Crunchbase), roughly double the level of prior years. Many of these were technology-related firms with limited customers and cashflow. We assume that 40% of this will end up in customer acquisition/digital marketing, with the majority going to key players such as Meta and Google. This level of spending may now normalise to more sustainable levels as we see new funding rounds dry up and many companies burn through cash reserves. This source of advertising spending will likely see a large drawdown, in turn prompting investors to reappraise their growth assumptions for the leading digital media players. We therefore do not consider these companies as illustrative of the Future Quality theme; notable downgrades are not a key attribute for enduring growth, and therefore we have no exposure in this area.

Within the Global Equity team, we believe ‘Future Quality’ companies should have long competitive advantage periods through which they can sustain high and/or improving cash returns. The challenge for investors is that only a fraction of companies within the global universe will display such characteristics.

For more information on the investment approach of Nikko AM’s Global Equity Team, and ‘Future Quality companies, please download their new investment guide here.

Footnotes:

[1] SPAC (special purpose acquisition company), FAANG (Facebook, Amazon, Apple, Netflix and Google), NFT (non-fungible tokens), FOMO (fear of missing out)

[2] Halgo (human algorithm)